Published: July 2025

Accounts receivable represents the money owed to your business by customers who have purchased goods or services on credit. Simply put, it's the outstanding invoices waiting to be paid. For Australian small and medium enterprises (SMEs), accounts receivable typically represents one of the largest current assets on the balance sheet, often accounting for 20-40% of total assets.

When you sell a product or service and allow the customer to pay later, you create an account receivable. This transaction increases your revenue immediately but delays the actual cash receipt. The time between the sale and payment collection is crucial for your cash flow management.

The accounts receivable cycle begins when you deliver goods or complete services for a customer and ends when you receive full payment. This process typically involves:

According to the Australian Small Business and Family Enterprise Ombudsman, payment delays are one of the most significant challenges facing small businesses, with the average payment time for small businesses extending to 26.4 days beyond agreed terms. Poor accounts receivable management can severely impact your business in several ways:

Cash Flow Disruption: Late payments create cash flow gaps that can prevent you from paying suppliers, staff, or meeting other operational expenses. The Reserve Bank of Australia reports that cash flow problems are the leading cause of small business failures.

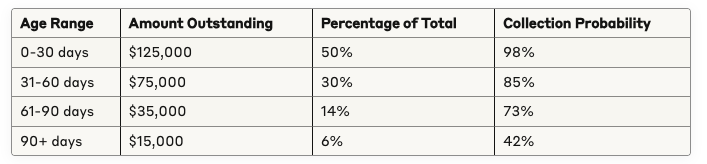

Increased Bad Debts: The longer an invoice remains unpaid, the lower the likelihood of collection. Industry statistics show that after 90 days, collection probability drops to approximately 73%, and after six months, it falls to just 42%.

Opportunity Cost: Money tied up in receivables cannot be invested in growth opportunities, inventory, or interest-bearing accounts. This represents a hidden cost to your business.

Administrative Burden: Chasing overdue payments consumes valuable time and resources that could be better spent on revenue-generating activities.

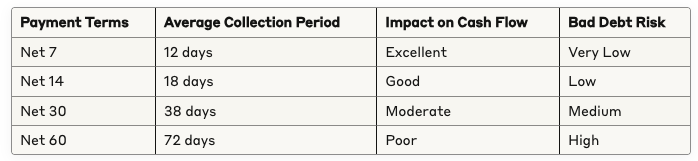

Australian businesses commonly use various payment terms that significantly impact accounts receivable management:

Net 30: Payment due within 30 days of invoice date. This is the most common term for B2B transactions in Australia.

Net 14: Payment due within 14 days, often used for smaller transactions or when faster cash flow is required.

Net 7: Payment due within 7 days, typically reserved for urgent services or cash-sensitive businesses.

2/10 Net 30: A 2% discount if paid within 10 days, otherwise full amount due in 30 days. This incentivises early payment and improves cash flow.

Table showing the relationship between payment terms and business outcomes

The choice of payment terms should balance customer relationships with cash flow needs. Shorter terms improve cash flow but may reduce competitiveness, while longer terms may attract customers but strain working capital.

Clear Invoice Details: Ensure every invoice contains complete information including invoice number, date, description of goods/services, payment terms, due date, and multiple contact methods.

Prompt Invoice Delivery: Send invoices immediately upon completion of work or delivery of goods. Delays in invoicing directly translate to delays in payment.

Professional Presentation: Use professional invoice templates that reflect your brand and make payment instructions clear and prominent.

Before extending credit to new customers, conduct thorough credit checks using services like Equifax or illion. Consider factors such as:

Implement a structured approach to following up on overdue accounts:

Day 1-7 Past Due: Friendly reminder via email or phone callDay 8-30 Past Due: Formal demand letter with payment deadlineDay 31-60 Past Due: Phone follow-up with payment arrangement discussionDay 61+ Past Due: Consider external collection agency or legal action

Early Payment Discounts: Offer discounts for prompt payment (e.g., 2% discount for payment within 10 days).

Late Payment Charges: Implement late fees in accordance with Australian Consumer Law. Typical charges range from 1.5% to 2% per month on overdue amounts.

Progress Payments: For larger projects, structure payments in stages to reduce exposure and improve cash flow.

Understanding how accounts receivable affects your cash flow is crucial for business planning. Here's how to calculate the impact:

DSO measures how long it takes to collect receivables on average.

Formula: DSO = (Accounts Receivable ÷ Total Sales) × Number of Days

Example Calculation:

A DSO of 30 days means customers take an average of 30 days to pay their invoices.

Table showing potential cash flow improvements from reducing DSO

These improvements represent one-time cash flow benefits that can be reinvested in the business or used to reduce borrowing costs.

Modern technology can significantly improve accounts receivable management efficiency:

Popular Australian accounting platforms like Xero, MYOB, and QuickBooks offer integrated invoicing and receivables management features including:

Offering multiple payment methods reduces friction and accelerates collections:

Specialised software can automate much of the collection process:

Australian businesses must comply with various regulations when managing accounts receivable:

The Competition and Consumer Act 2010 governs business-to-consumer transactions and limits the fees and charges that can be imposed for late payments.

For businesses selling goods on credit, registering security interests under the PPSA can provide protection in case of customer insolvency.

When collecting debts, businesses must comply with privacy laws regarding the collection, use, and disclosure of personal information.

This office provides mediation services for payment disputes and has established a voluntary Payment Times Reporting Scheme to improve payment practices.

Different industries face unique accounts receivable challenges:

The Security of Payment legislation in each Australian state provides specific rights and procedures for recovering payments. Progress payments and retention amounts are common, requiring careful contract management.

Service businesses often struggle with scope creep and disputed invoices. Clear engagement letters and regular progress billing help minimise these issues.

While many transactions are cash-based, B2B sales (to other retailers or corporate clients) require careful credit management due to the industry's generally low margins.

Long production cycles and large order values create significant receivables exposure. Credit insurance may be worthwhile for major customers.

Divide customers into categories based on payment behaviour:

Premium Customers: Excellent payment history, minimal follow-up requiredStandard Customers: Generally pay on time, occasional gentle reminders needed

Problem Customers: Regular late payments, require intensive managementHigh-Risk Customers: Consider cash-on-delivery or credit limits

Table showing typical aging analysis for Australian SME accounts receivable

This analysis helps prioritise collection efforts and estimate bad debt provisions.

For businesses with significant receivables, factoring can provide immediate cash flow:

Costs typically range from 0.5% to 3% per month, but the improved cash flow often justifies the expense.

Key performance indicators for accounts receivable management include:

Inadequate records make collection difficult and may prejudice legal proceedings. Maintain comprehensive files including contracts, delivery confirmations, correspondence, and payment history.

Sporadic collection efforts signal to customers that prompt payment isn't important. Consistent, professional follow-up establishes expectations and maintains relationships.

Offering payment terms without proper credit evaluation increases bad debt risk. Even small customers should undergo basic credit checks.

Changes in customer payment patterns often indicate financial difficulties. Address issues early rather than waiting for accounts to become severely overdue.

Personal relationships with customers can cloud business judgment. Maintain professional standards and treat all customers fairly regardless of personal connections.

Sometimes external assistance is necessary:

Licensed collection agencies can pursue difficult accounts while maintaining your customer relationships. Fees typically range from 15% to 35% of collected amounts.

For significant debts, legal proceedings may be necessary. Consider factors such as:

Specialists can help design systems, train staff, and provide ongoing support for complex receivables management challenges.

Every business should have a written credit policy covering:

AI is increasingly being used to predict payment behaviour, optimise credit decisions, and automate collection activities. Small businesses can access these capabilities through cloud-based platforms.

While still emerging, blockchain technology could revolutionise invoice processing and payment verification, reducing disputes and accelerating collections.

Australia's Consumer Data Right enables better credit assessment through access to real-time banking data, improving credit decisions and reducing bad debts.

Environmental, social, and governance (ESG) considerations are influencing B2B payment terms, with some companies offering better terms to suppliers with strong sustainability credentials.

Accounts receivable is money that customers owe your business for goods or services you've already delivered but haven't been paid for yet. It appears as an asset on your balance sheet because it represents money you have the right to collect.

Start following up immediately when an invoice becomes overdue. Send a friendly reminder on day 1, a formal notice by day 7-10, and make phone contact by day 30. The sooner you start, the better your chances of collection.

Yes, but only if your terms and conditions specifically allow it and the charges are reasonable. Interest rates of 1.5% to 2% per month are generally considered acceptable. Ensure your terms comply with Australian Consumer Law for consumer transactions.

DSO varies by industry, but generally 30-45 days is considered reasonable for most Australian SMEs. Construction and professional services often have longer DSO due to industry practices, while retail businesses should target much shorter periods.

Consider writing off debts when collection costs exceed the debt amount, the customer is insolvent, or the debt is more than 12 months overdue with no payment activity. Consult your accountant about tax implications and timing.

No, businesses can collect their own debts without a licence. However, if you engage a third party to collect debts on your behalf, they must hold an appropriate Australian Credit Licence or debt collection licence depending on the jurisdiction.

Focus on shortening payment terms where possible, offering early payment discounts, improving your invoicing process, implementing systematic follow-up procedures, and using technology to automate routine tasks. Even small improvements in DSO can significantly impact cash flow.

Include your business name and ABN, customer details, invoice number and date, clear description of goods/services, payment terms, due date, amount due, and multiple payment methods. Make payment instructions prominent and easy to follow.

Early payment discounts can be effective if the cost is less than your borrowing rate or if improved cash flow creates other opportunities. A 2% discount for payment within 10 days (instead of 30) effectively costs about 37% annually, so ensure the benefits justify this cost.

Implement a customer classification system and adjust terms for chronic late payers. Consider requiring deposits, shorter payment terms, or cash on delivery. Document all interactions and consider whether the customer relationship is profitable given the collection costs and cash flow impact.

Accounts receivable is money customers owe you (an asset), while accounts payable is money you owe suppliers (a liability). Both are crucial for cash flow management, but they appear on opposite sides of your balance sheet.

Accounts receivable financing (factoring or invoice discounting) allows you to borrow against your outstanding invoices. You can either sell invoices to a factor at a discount or use them as security for a loan. This provides immediate cash flow but costs typically range from 0.5% to 3% per month.

Sydney Bookkeeper provides bookkeeping services for Australian SMBs, including accounts receivable management through invoice processing, sending overdue reminders, allocation of remittances, and customer collections reporting to assist with cash flow monitoring and collections. Our offerings also include weekly and monthly reconciliations, bank account and card allocations, GST mapping, data entry, and BAS/IAS assistance for ATO compliance.

Additional services encompass financial reporting such as profit and loss reviews, balance sheet reviews, monthly cash flow reviews, margin analysis, and interim financial reporting, along with payroll management involving employee onboarding, salary calculations via Xero, payslip distribution, and PAYG support. We offer Xero setup, migration, training, and books catch-up for backlogged records. Services can be fully or partially managed, with flexible options to collaborate with in-house teams, no lock-in contracts, and pay-for-what-you-use pricing. Onboarding begins with a free assessment and customised proposal. For more details, visit our website at www.sydneybookkeeper.com.

sydney bookkeeper offers expert bookkeeping services sydney-wide for business owners, finance managers, and accounting firms to fuel local business growth.our sydney team delivers affordable packages, including professional bookkeeping, invoicing, payroll, and xero services.

from reconciliations to bas and xero setup, we ensure ato compliance, cut costs, and automate tasks, helping you scale confidently without long term contracts.perfect for businesses throughout sydney seeking reliable, local support.

ready to simplify bookkeeping and focus on growth?

our sydney bookkeeper experts will assess your needs and show how much time and money you can

save with our tailored services. no lock-in contracts.

pay only for what you use and pause anytime.